After “Understanding Value” in Part 1, and “Creating Value” in Part 2, we come to the third aspect of the value journey, “Capturing Value”. When we think of capturing value, the topic of pricing comes up as important. While price is an important aspect of capturing value, it is not the only one. The price of the product allows capturing value in the economic sense.

The more important and strategic questions to ask are:

1. What is the industry and competitive landscape that presents the opportunity to capture value?

2. What is the product strategy and business model so that we can continue to capture value over time?

3. What unique differentiators will allow us to capture value better than the competition?

Thus, business strategy is at the very heart of capturing value. As we did in earlier parts, we will look at this from the lens of Apple and the insanely great product manager, Steve Jobs. Here we will take the example of the iPod and the music business.

Industry & Competitive Landscape

As we all know, the iPod was not the first music player in the market. There were different categories of companies – digital music management software or jukebox companies (Real, Microsoft, MusicMatch, etc.), digital music player companies (Creative, SonicBlue, Sony, etc.), the recording labels (Warner, Universal, etc.), all of which did not understand, let alone communicate or collaborate with each other. There were different business models, ranging from music subscription services to free illegal downloads. The market was very fragmented, and the industry was in a very confused state.

So why did Apple choose to enter the music business?

Well the question Apple asked circa 2001 was different. The question was, how can the Mac become more valuable for its users. At MacWorld in 2001, Steve Jobs outlined Apple’s digital hub vision, talking about the digital revolution and the growth in digital devices like cameras, camcorders, music players and DVD players – and how the Mac would be the hub of the digital lifestyle.

“Mac can become the “digital hub” of our emerging digital lifestyle, adding tremendous value to our other digital devices.”

Before Apple launched the iPod, Apple launched iTunes at MacWorld in Jan 2001. It gave away iTunes for free, just like it did with iMovie and iDVD. The thinking, presumably, was that it was important to capture value from increased sales of the Mac platform that had all these apps bundled in, rather than trying to capture value from apps that people might or might not purchase. In addition, even while Apple was working on iTunes it had recognized the importance of creating a digital music player as accompanying hardware that would represent a potential higher opportunity of capturing value in the music category.

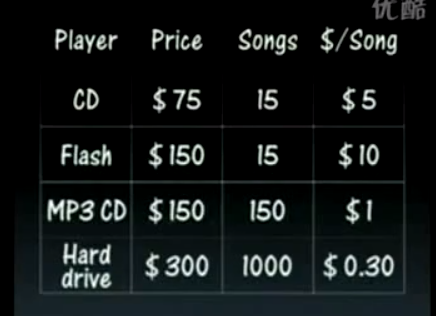

While Robbin was working on iTunes, Jobs and Co. started looking for gadget opportunities. They found that digital cameras and camcorders were pretty well designed and sold well, but music players were a different matter. “The products stank,” Greg Joswiak, Apple’s vice president of iPod product marketing, told Newsweek. Digital music players were either big and clunky or small and useless. Most were based on fairly small memory chips, either 32 or 64 MB, which stored only a few dozen songs — not much better than a cheap portable CD player.

In Oct 2001, when Steve Jobs announced the iPod, he took stock of the music players on the market, and summarized the landscape in the following slide, and said that Apple had decided it wanted to be in the Hard-drive music player category.

Over the next few years, Apple’s success attracted other companies to enter the market, namely, Sony, Dell, Microsoft and continued innovation by Creative, iRiver to create cheaper music players, however, a lower priced product could not stop the iPod juggernaut.

Product Strategy & Business Model

Apple’s product strategy and business model evolved in a rapid manner that enabled it to increase the value it captured in the music industry. It went through different phases.

Phase 1 – Focus on the Mac (2001 – 2002)

The first iPod supported Firewire to transfer music to it, and Firewire was only available on the Mac. iTunes was also available only on the Mac. Even though the iPod was the most expensive music player on the market, the product itself fit into a bigger “digital hub” strategy for the Mac. In that sense, the business model was only about hardware unit sales.

Phase 2 – iPod Expansion (2002 – 2004)

In the second phase of the product strategy and business model, three important decisions were made:

1. Supporting Windows – “Hell Froze Over”

This was perhaps one of the most significant milestones in the product strategy, perhaps a recognition of the fact that the iPod and Music were a legitimate standalone business in their own right, instead of only being leveraged to spur Mac sales.

The biggest risk was that we saw people buying Macs just to get their hands on iPods. Taking iPods to Windows – that was the big decision. We knew once we did that that we were going to go all the way. I’m sure we’re losing some Mac sales, but half our sales of iPods are to the Windows world already.

(Steve Jobs’ interview in Rolling Stones, 2003)

2. iTunes Music Store

In July 2003, Apple announced the iTunes Music Store in partnership with all the five major record labels, after intense discussions. Prior to this, as noted earlier, the record labels were all hurting from the piracy of music enabled by peer to peer sharing sites like Napster, Kazaa, etc. Apple convinced the record labels that it provided the only legal alternative to consumers of owning digital music.

At first, they kicked us out. But we kept going back again and again. The first record company to really understand this stuff was Warner. Next was Universal. Then we started making headway. And the reason we did, I think, is because we made predictions. And we were right. We told them the music subscription services they were pushing were going to fail. MusicNet was gonna fail. Pressplay was gonna fail. Here’s why: People don’t want to buy their music as a subscription. They bought 45s, then they bought LPs, they bought cassettes, they bought 8-tracks, then they bought CDs. They’re going to want to buy downloads. They didn’t see it that way. There were people running around – business-development people – who kept pointing to AOL as the great model for this and saying, “No, we want that – we want a subscription business.” Slowly but surely, as these things didn’t pan out, we started to gain some credibility with these folks.

Our position from the beginning has been that eighty percent of the people stealing music online don’t really want to be thieves. But that is such a compelling way to get music. It’s instant gratification. You don’t have to go to the record store; the music’s already digitized, so you don’t have to rip the CD. It’s so compelling that people are willing to become thieves to do it. But to tell them that they should stop being thieves – without a legal alternative that offers those same benefits – rings hollow. We said, “We don’t see how you convince people to stop being thieves unless you can offer them a carrot – not just a stick.” And the carrot is: We’re gonna offer you a better experience… and it’s only gonna cost you a dollar a song.

The other thing we told the record companies was that if you go to Kazaa to download a song, the experience is not very good. You type in a song name, you don’t get back a song – you get a hundred, on a hundred different computers. You try to download one, and, you know, the person has a slow connection, and it craps out. And after two or three have crapped out, you finally download a song, and four seconds are cut off, because it was encoded by a ten-year-old. By the time you get your song, it’s taken fifteen minutes. So that means you can download four an hour. Now some people are willing to do that. But a lot of people aren’t.

Apple also convinced the labels that in the online world, consumers should be able to buy the songs they liked individually instead of downloading the entire album, which is how music is sold on CDs, and that each song should be sold for $0.99.

Thus the business model got a new dimension of content sales, in addition to hardware sales. This was a far more lucrative element of the business model as compared to hardware sales, just due to the sheer number of songs that people would want to download and own in their music libraries. Not surprisingly, in one year after launch of the iTunes Music Store, Apple had sold over 70 million songs.

3. Product Line Expansion

The third aspect of the product strategy in this phase was about expanding the product portfolio to create different product variations to capture value based on preferences for color, capacity and form.

The first product line expansion was the iPod Mini. Over time Apple created the iPod nano, iPod Shuffle as additional product lines, and in more recent years, the iPod Touch.

Phase 3 – Beyond Music (2004 – 2006)

In the third phase of the iPod product strategy and business model, Apple expanded the iPod function to reach beyond music, moving into photos, videos and games. New models, like the iPod nano and iPod Shuffle were introduced. The iPod and iTunes Music Store also saw a huge increase in geographic reach during this period, reaching all parts of the world. The ecosystem of third party accessory providers created additional opportunities for capturing value.

Apple also delved into testing integration with the mobile phone through the partnership with Motorola, to create the Rokr as the first non-Apple device to work with the iTunes Music Store.

This was a period where Apple continued its growth phase and extended its dominance over the industry.

The business model expanded along hardware sales to include new models, along content sales to include new content types (videos, movies, TV shows, ringtones, etc.), and along accessories sales (dock-based accessories, headphone-jack based accessories, AppleTV, Nike+, etc.)

Unique Differentiation

Apple completely changed the music industry with iTunes and the iPod. And in doing so, it leveraged its core competencies that we outlined in earlier parts:

1) Simplicity and beauty in design, and

2) Hardware and software that work seamlessly together.

As mentioned earlier, the music industry was in a quagmire. There were different categories of companies – digital music management software companies, digital music player companies, the recording labels, all of which did not understand, let alone communicate or collaborate with each other. There were different business models, ranging from music subscription services to free illegal downloads.

This was a perfect storm for Apple to leverage its competencies in hardware, operating system, application software, Internet services, and design.

“Design is not just how it looks and feels like. Design is how it works.”

Many other companies entered the fray looking at Apple’s success, most notably Microsoft with Zune. However, none of them could hold Apple back. There were technological and product advantages, there was the amazing marketing machine, but at the end of the day, it was the complete solution that was born out of really understanding people’s love for music, and how specially their music must be treated.